The Truth About the 50-Year Mortgage: Pros, Cons & What Buyers Need to Know

- Hennigan Realty

- Nov 14, 2025

- 3 min read

As housing affordability becomes a national concern, the idea of a 50-year fixed mortgage has started making headlines. Supporters claim it can help buyers lower their monthly payments and finally break into high-priced housing markets. But longer mortgage terms come with major trade-offs most buyers don’t fully understand.

Before forming an opinion, here’s a clear breakdown of what a 50-year mortgage actually means for buyers — the benefits, the risks, and how it compares to a traditional 30-year mortgage.

✅ What Is a 50-Year Mortgage?

A 50-year mortgage is exactly what it sounds like — a home loan paid off over 600 months instead of the traditional 360.The longer term lowers the monthly payment, but also stretches your interest costs dramatically.

This loan type is rare in the U.S. but has been proposed as a possible solution to housing affordability challenges in high-cost states.

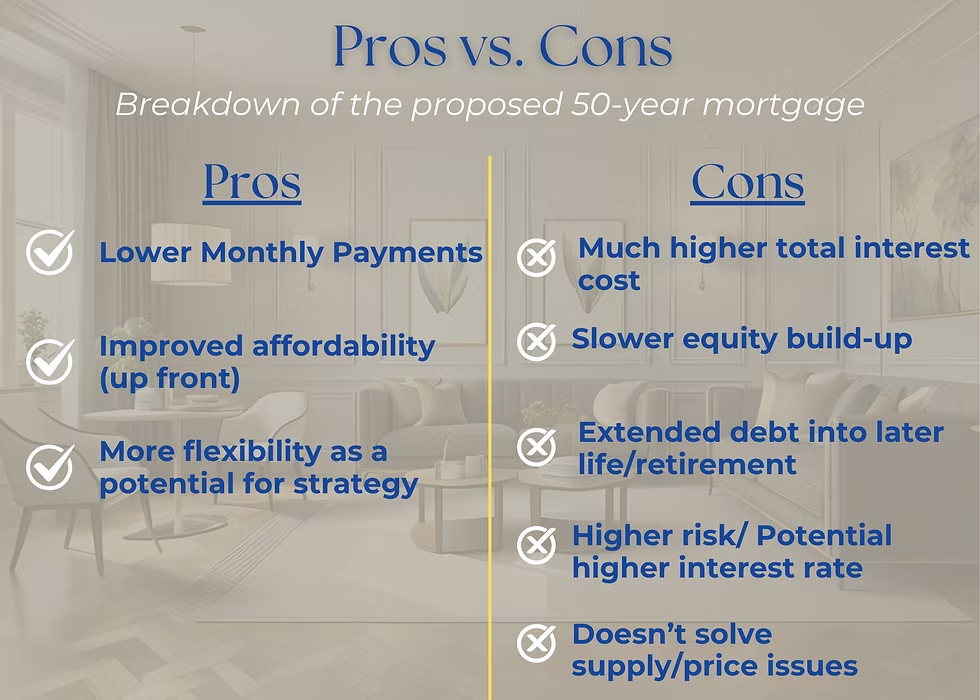

Pros of a 50-Year Mortgage

1. Lower Monthly Payment

This is the biggest selling point. A longer amortization period spreads out the loan, resulting in a much lower monthly payment — meaning more breathing room in your budget.

2. May Help Buyers Qualify Sooner

Because the payment is lower, your DTI (debt-to-income ratio) decreases. This can help more buyers qualify for a loan who otherwise wouldn’t get approved under a 30-year payment structure.

3. More Flexibility in the Early Years

Some buyers may use a 50-year mortgage as a strategic entry point. With a lower payment, buyers could choose to:

Pay extra principal

Refinance later

Sell or move before the full loan term

The key advantage is optionality — the required monthly payment is smaller, giving buyers more choices upfront.

Cons of a 50-Year Mortgage

1. Much More Interest Paid Over Time

This is the biggest drawback — and it’s a massive one. The longer the mortgage, the more interest you pay, and with a 50-year mortgage, you’re paying interest for two generations worth of time.

2. Equity Builds Much Slower

Because early payments mostly go toward interest, you build equity at a much slower pace. With a 50-year mortgage, buyers may not see principal-heavy payments until years 20–30. For comparison:📉 On a 30-year loan, the shift toward principal typically begins around years 10–15.

This slow equity growth can become a major problem if you need to sell or refinance.

3. You May Carry a Mortgage Into Retirement

If you take out a 50-year loan at age 30, you will still be making payments at age 80.This can drastically affect:

Retirement planning

Paying off debt

Long-term financial stability

Your ability to downsize or relocate later in life

4. Higher Interest Rates & Higher Risk

Lenders may charge a higher rate for a 50-year mortgage because they view long-term loans as higher-risk. Additionally, if home prices decline or your life circumstances change early in the loan, selling or refinancing may be more difficult due to lower equity.

5. Doesn’t Solve Housing Supply or Price Issues

A longer loan term doesn’t fix the real problem: limited housing supply and high prices. In fact, it may even make prices rise because:

More people can suddenly “afford” homes

Demand increases

Sellers raise prices

Inventory tightens

This could mirror the price boom during the COVID housing market.

50-Year Mortgage vs. 30-Year Mortgage: Equity Timeline

Mortgage Type | When Payments Shift From Mostly Interest to More Principal |

30-Year Loan | Around 10–15 years |

50-Year Loan | Around 20–30 years |

This difference alone has a major impact on long-term wealth building.

Bottom Line: Is a 50-Year Mortgage Right for You?

A 50-year mortgage can make monthly payments more manageable — and in some cases, help buyers purchase a home they otherwise couldn’t. But the trade-offs are significant:

✔ Lower monthly payment

✘ Higher total cost

✘ Slower equity

✘ Longer financial commitment

✘ Higher risk in early years

Before choosing this route, sit down with a real estate professional and ask: “What will I owe after 10 years? After 20? How does this compare to a 30-year mortgage?”

Don’t just chase the lower payment. Think about long-term wealth, ownership, and financial freedom.

Comments